Executive’s lifestyle under scrutiny as duped investors wait for money

Christopher and Connie Brogdon’s asset list suggests the pinnacle of Atlanta prosperity.

The couple’s $5 million residence near the top of the St. Regis offers stunning views from one of Buckhead’s most elite addresses. They can pick from a Lexus SUV, a BMW coupe and a Porsche Panamera to navigate the city’s traffic.

For trips, they have the King Air private plane worth $1.5 million, and for leisure there’s the $2 million beach house on St. Simon’s Island.

Christopher Brogdon is a national player in the nursing home and assisted living industry, as well as being an owner of the J. Christopher’s restaurant chain. The 69-year-old businessman’s lifestyle could reflect hard-earned success.

But today, his riches have emerged as symbols of excess in a federal case that accuses Brogdon of funding this lifestyle through fraud. Brogdon’s career has been marred, at several points, by charges of wrongdoing — including allegations of poor care to frail elderly people. He’s slipped out of the noose of allegations in the past — or remade himself.

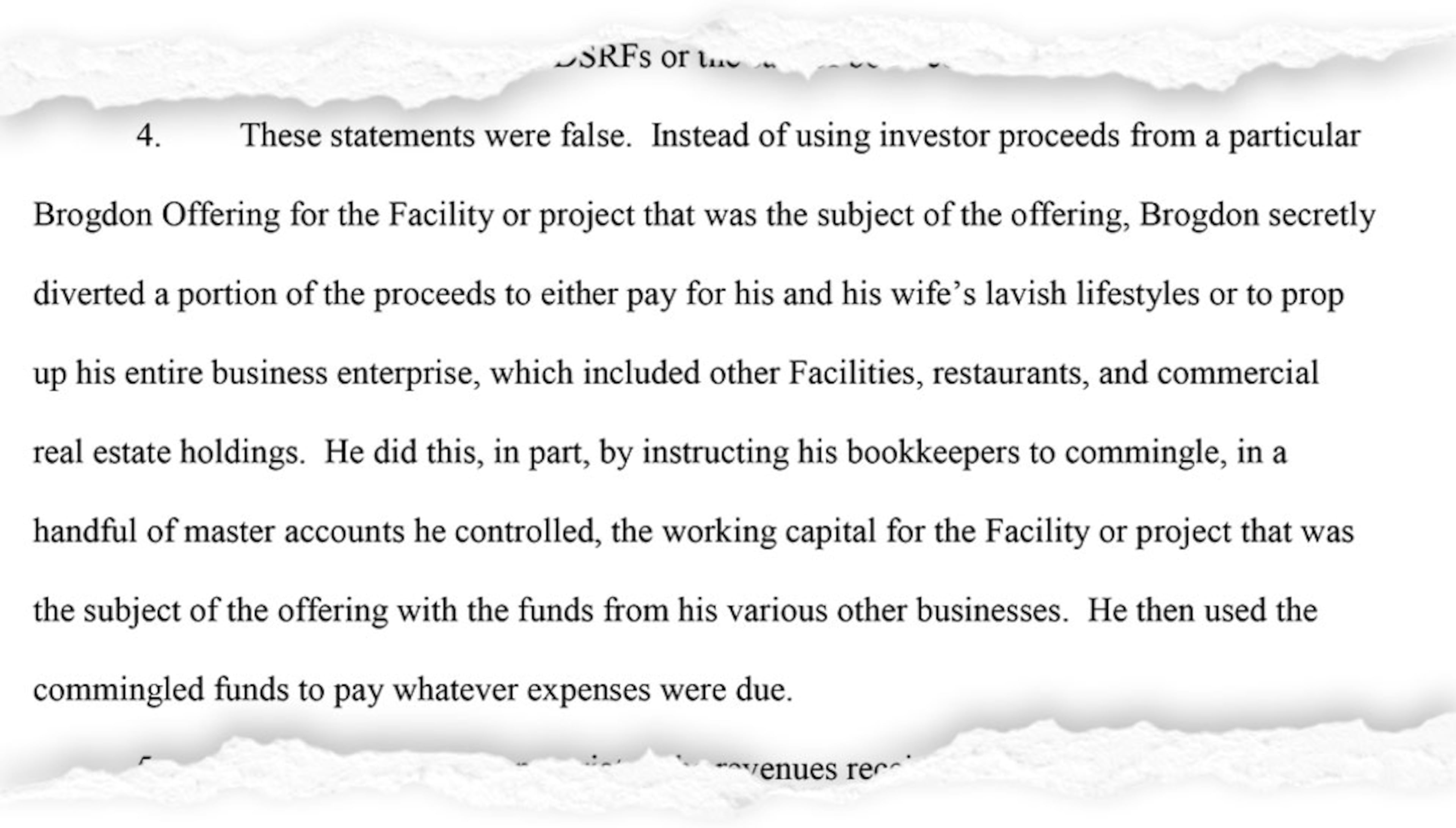

Now, the Securities and Exchange Commission is bearing down on Brogdon. The SEC accused him of fraud in its 2015 civil case and a court ordered that $89 million be paid to trusting investors in his nursing home or assisted living deals. Brogdon diverted bond cash for other purposes, the SEC charged, including moving money from one assisted living or nursing home project to another and funding his family's high-end lifestyle. The SEC also accused brokers who sold the bonds of misleading investors — many of them retirees.

The details of what happened in these bond deals and what took place inside some of his facilities offer an example of how the long-term care business can profit by taking advantage of both naive investors and elderly people who need 24-hour care.

Attorneys representing Brogdon in the SEC case declined an interview request from The Atlanta Journal-Constitution, and Brogdon did not respond to phone messages.

A federal judge in New Jersey is scheduled to hear arguments later this month about whether Brogdon should get an extension of his deadline to come up the millions he still owes. Brogdon argues that re-setting the deadline to the end of next year will allow him to get higher prices for the assets, resulting in more money for the investors.

However, the SEC questions Brogdon’s sincerity and says his projections of the money he can bring in have fallen far short. Plus, the SEC says he’s intentionally delayed selling off his homes and other assets, while continuing to find the cash to spend $100,000 a month on the family budget.

Brogdon’s critics say it’s no surprise that the SEC is having a hard time getting the money.

“He is a con man who cheats investors at the expense of assisted living and nursing home residents,” said Florida attorney Jim Wilkes, whose firm filed a lawsuit this year accusing a bank of enabling Brogdon to carry out what it calls a massive healthcare scheme. “He’s got a history that goes back 30 years.”

Betrayed investors

Cori Ribaudo and her husband, Tom, never met Brogdon. But their financial futures became tied to Brogdon’s business deals after they went to a free, broker-sponsored lunch at a Golden Corral restaurant near their home in The Villages, a golf-cart oriented retirement community in Florida that is filled with affluent retirees.

The sales pitch made sense to the Ribaudos. Bonds seemed like a secure choice for some of their retirement nest egg, and the interest payments would give them income and tax benefits. The investment company pitching the bonds said they were an ultra-safe investment. “We were guaranteed we would never lose the money – guaranteed — and that’s what kills us,” Cori Ribaudo said.

The couple had mostly invested in real estate over the years, so they asked a lot of questions, wanting to make sure their money would be secure. “They lied,” Ribaudo said.

The couple lost a chunk of their savings in various bond deals recommended by Lawson Financial, the firm that hosted the Golden Corral lunches. Lawson has since been sanctioned and kicked out of the securities industry for misleading clients and misusing their funds. "We've probably lost a fourth of our life savings," Ribaudo said.

The Brogdon-related bonds that the Ribaudos invested in were “conduit municipal bonds.” Those are bonds that are authorized by a government authority but not guaranteed by the government. They’re a way for private companies or non-profits to get financing for projects that might have some public benefit. Hospitals, nursing homes, retirement communities and colleges often raise money for projects through conduit bonds.

Investors benefit because money they make from interest payments isn’t taxed and returns are usually higher than what government bonds pay. But if the private project fails, investors can come out with nothing or just a fraction of what they invested.

In the case of the Brogdon bonds, the SEC found that brokers and the bank involved in the deals failed to protect investors, as they were obligated to do, especially when it came to notifying investors of risks and of Brogdon’s failures on earlier projects. By failing to disclose problems, they paved the way for him to do more bond deals, the SEC found.

The Brogdons are now under a court order to pay off the principal and interest owed in 13 bond offerings and 6 private placements offerings that raised money for the projects. The court order includes a list of assets to be sold to help pay off the debts, but the Brogdons are obligated to use personal assets, too, if needed.

The plan called for everything to be paid off by the end of this year, but the court-appointed monitor estimated in a recent report that Brogdon will fall $20 million short. One reason there isn’t enough money to pay back the wronged investors, the monitor reported, is the “perpetuation by Mr. Brogdon of a lavish lifestyle.” The monitor also said that Brogdon prices his assets so high that many properties aren’t selling.

Brogdon said in court filings that the monitor’s hefty billings are hurting his plan. He said he is marketing his homes, airplane and his stake in J. Christopher’s restaurants, as well as facilities that are pledged to be sold for the plan.

In a filing asking the judge in the SEC case to grant more time for him to market assets, he objects to criticisms from those who claim he is stalling. “In business, hurdles and obstacles arise in the ordinary course,” Brogdon wrote. “To be successful, one has to look for solutions, not places and people to blame. The solution here is to continue to market the assets and to work hard on maximizing their value for the benefit of the investors.”

Ribaudo said she would love to get back what she and her husband have lost. But she’s not holding her breath that the SEC’s action will make them whole. The experience changed her outlook about where to park her money and left her wary about the investment industry. “I will never invest in bonds again,” she said.

Checkered history

The SEC case is not the first time Brogdon’s career has been threatened by regulators.

Four decades ago, Brogdon was a broker and by 1984 found himself in serious trouble. First an industry regulator found he made unauthorized transactions in a customer’s account “for his own nefarious purposes.” That same year, he was also accused of devising a scheme to circumvent a limit on financing.

In both cases, he was censured, fined and barred from working as a broker again.

Brogdon then remade his career in the long-term care industry.

Between 1992 and 2014, he bought or renovated at least 60 nursing homes, assisted living facilities or retirement housing developments, according to the SEC’s complaint. Brogdon got money for his projects through bonds authorized by local authorities, private financing or banks. Brokers he had relationships with would sell the bonds, often to unsophisticated investors, bringing in cash for the projects and fees for themselves.

In a 1993 article with the headline “Hello, sucker,” Forbes magazine highlighted Brogdon’s bond deals, saying “sleazy brokers” enticed novice investors with high-yield bonds that they assumed were safe but, in fact, were shaky. In spite of the attention, the bond projects continued to get approved by the local authorities and sold by the brokers.

It didn’t take long before regulators questioned the quality of care at some facilities operated by Brogdon companies.

Nearly 20 years ago, a Florida prosecutor announced the arrest of five people and three corporations in a nursing home abuse case. When announcing the charges in 1999, prosecutor Rod Smith said the five people accused in the case will not “have anything to do with taking care of elderly people again,” according to news coverage of the arrests.

Brogdon was among those arrested and accused of racketeering, elder abuse, Medicaid fraud and theft. But the criminal charges against Brogdon and the others were dropped once a corporate consent order was reached, according to Florida records obtained by The Atlanta Journal-Constitution. A new company that had taken over was improving care, according to the records. The companies involved agreed to a $377,000 fine and pledged to deliver quality care to nursing home residents.

Nursing home wounds

When the Florida regulators were building a case against Brogdon, they were in touch with Georgia officials who were also investigating the executive in connection with suspicious bond deals, billing practices and quality of care, according to records of the Florida investigation obtained by the AJC. With the Florida case settled, however, nothing stopped Brogdon from continuing to expand.

"One of the things that bothered me was that Chris Brogdon was, in effect, run out of the state of Florida for neglecting elderly residents in his facility and yet the state of Georgia welcomed him here and enabled him to establish long-term care facilities here," said John Suthers, a Savannah attorney whose practice includes nursing home abuse cases.

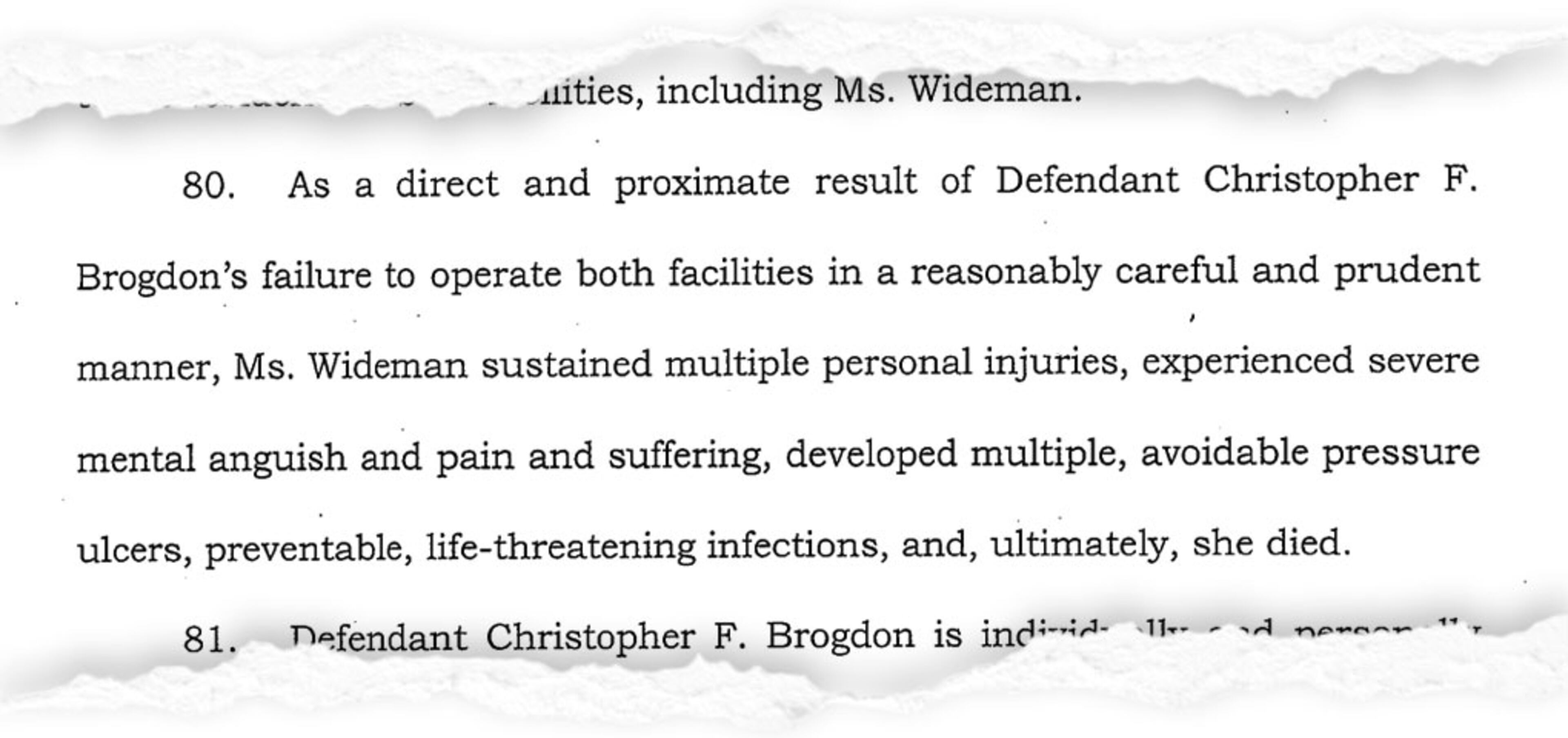

Suthers represented the family of Ermyne Ann Wideman, who died in 2004 after residing at Shadowmoss Plantation and Sandsprings Landing, elder-care homes owned by Brogdon-controlled companies.

Wideman suffered multiple falls at Sandsprings Landing and became completely dependent on staff. When she could no longer afford Sandsprings, the staff convinced Wideman’s family to move her to Shadowmoss, saying the facility could meet her care needs and that the facility “specialized” in caring for residents in the same condition — which the lawsuit says were false representations. Shortly after coming to Shadowmoss in April 2004, Wideman began developing bed sores, a threat to patients with limited mobility if staff members do not turn the patients frequently.

The sores grew worse and then were not treated properly, the lawsuit said. Wideman died months later — in October 2004 — of infections from the multiple sores. State inspections found repeated violations at the home and concluded that Shadowmoss neglected Wideman. The facility wasn’t equipped to care for her in the first place, the state found.

The lawsuit also accused Brogdon of a pattern of opening long-term care facilities and enticing families to place loved ones in personal care homes — which are assisted living type facilities — that couldn’t provide the level of medical and personal care residents needed. The homes would be owned by shell corporations with no assets and would have no liability insurance as part of a scheme to avoid the costs of abuse lawsuits, the lawsuit said.

Suthers said the case was settled right before it was to go to trial.

Other lawsuits have also accused Brogon of avoiding liability by playing a corporate shell game.

A Tennessee judge awarded a $5 million judgment in 2010 in a lawsuit that alleged a resident of a Brogdon home suffered injuries that included dehydration, weight loss, malnutrition, two sexual assaults, six falls, skin tears, pressure sores, urinary tract infections, urosepsis and other health problems. To avoid paying, the nursing home ownership was transferred repeatedly to other entities, all controlled by Brogdon, according to a lawsuit filed this spring by Wilkes’ firm.

While the family prevailed, the shell game kept the deceased woman’s relatives from collecting any money.

Cash crunch

While the SEC is making an aggressive play for Brogdon’s assets, so are plenty of other creditors.

They are as big as the Internal Revenue Service, which is trying to collect $1.4 million, and as small as Performance Food Group. The commercial food supplier filed a lawsuit in Fulton County in June saying one of Brogdon’s companies stiffed it for more than $40,000 in orders at seven senior care facilities in Georgia, Alabama and Florida. The Brogdons have had accounts garnished, and they temporarily went into bankruptcy last year after a creditor was on the verge of seizing all of their household goods, including jewelry, artwork and a wine collection, from the St. Regis.

The cash crunch raises questions about whether Brogdon’s business entities have the cash flow to adequately take care of residents and pay staff.

Even with all the money owed, Chris and Connie Brogdon are continuing to cover their sizable monthly expenses. Those includes $22,000 a month in mortgage payments and other costs for their home at the St. Regis and $12,000 a month for the beach house.

They spend $20,000 a month for their private plane, according to the filings in the SEC case, which Brogdon argues helps him make the necessary trips to oversee facilities in Oklahoma. They even pay $1,500 a month for a daughter’s mortgage and $15,000 every quarter for Christopher Brogdon’s $6 million term life insurance policy.

Some who have studied the executive’s history say this case looks like more of the same, and they wonder if Brogdon will eventually escape SEC oversight and continue with business as usual.

"This man is a common thief," said Wilkes, the Florida attorney. "He has stolen a couple of hundred million dollars and he has committed securities fraud and he has done it over and over and he gets away with it. At some point, the courts have to get outraged."

DEALS INCLUDED IN COURT ORDER

Christopher Brogdon raised money to buy or renovate nursing homes, assisted living and retirement communities through bond offerings approved by local government authorities in several states. Brokers sold the bonds to investors with promises of relatively high interest payments that would not be taxed. Brogdon also secured financing through other high-return securities marketed to investors. But the Securities and Exchange Commission said Brogdon deceived investors, co-mingling money that was supposed to be dedicated to specific projects and diverting funds to other business ventures and to family accounts. Now, he is under a court order to pay investors the interest and principal owed in 13 bond deals and six private placement offerings: