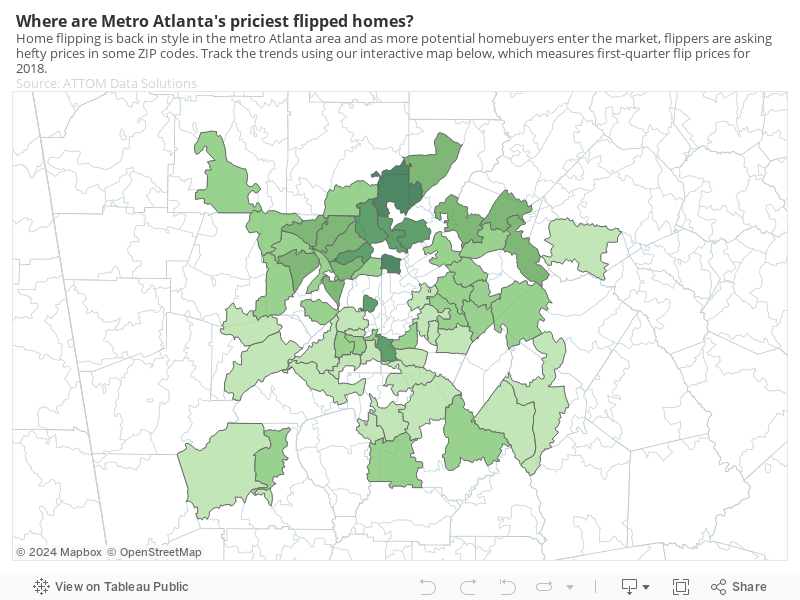

Home flipping once again on the rise in metro Atlanta

The three-bedroom house on hill on Sherbrooke Drive – east of I-85, west of Northlake – was built in the 1960s. But it’s been transformed by Greg Mortimer’s contractors.

Columns in front were swapped out. Walls were removed to open up the kitchen. New counters were installed, appliances replaced, a back deck rebuilt, the yard landscaped.

Mortimer and his brother bought the home in June for $330,000. After $100,000 in improvements, they plan to list it Friday at $535,000 to $550,000.

“You get in, you get out,” he said. “There’s risk. But you have to know what you are buying, what you are getting into. And you have to have good people around you.”

A dozen years ago, house-flipping — the trend of investors buying up homes, making surface improvements, then expecting to sell quickly and make a killing — reached a frenzy. It was partly blamed for real estate's overheating and ultimate collapse — and the national disaster that followed. But after virtually disappearing, flipping is on the rise again.

There were more than 1,400 house-flip sales in metro Atlanta during the first quarter of this year, up 36 percent from three years ago, according to Attom Data Solutions.

An Atlanta-based company is keenly aware of the resurgence — and has come up with a new way for flippers to borrow for their projects, while giving individuals a way to invest small amounts of money.

But this time, it's different for those looking to make a profit off the houses they've bought: Buyers must be more selective and invest more money in the property, said Brian Dally, chief executive and co-founder of Groundfloor, which loaned the Mortimers money to help buy and renovate the Sherbrooke Drive property, as well as others.

“Here’s what I know: The percentage of loans that is going to renovation has doubled,” Dally said. “You have to be more capable, more talented, to be successful.”

Groundfloor has loaned $70 million across 500 properties in the United States, one-third of them in Atlanta. The company an unusual – if not unique – model for lending: Small investors put money into a fund that is loaned to flippers for six to 18 months. The investors, who can choose which project they want their money to go to, can toss in as little as $10.

The borrower pays the company a fee, typically $6,000 to $12,000 per loan. The flipper gets an average of $150,000. And the small investors on average make about a 12 percent return, although about 2 percent of borrowers don’t pay the loan back, Dally said. “We freely admit there’s risk. If there’s no risk, there’s no investment.”

The housing bubble burst in Atlanta after years of frenetic homebuilding. Even with low-standard – and even criminally inaccurate – loans, there were just far too many houses for the number of people able to afford one.

Now, home sales are not booming, just home prices. And that means flips serve a different role, Dally said: Renovation is cheaper than building new houses. Unlike the over-supply of the housing bubble, metro Atlanta now has a shortage of homes.

Every time flippers renovate a vacant house, they add to supply, he said. “What is different is the source of pricing demand, a generational shift back toward home ownership.”

Groundfloor is not adding any instability in the market, Dally said. “Here is what didn’t cause the housing crisis: Individual investors putting $10 into investments in real estate.”

It had been extraordinarily easy to get loans during the years of the housing bubble. After the bust, it became nearly impossible, said John Mangham, a longtime real estate manager, investor and, more recently, a flipper. He got a loan from Groundfloor for a house in Adair Park when prices were depressed, but banks were loath to loan money on housing.

“We looked at depressed prices and saw opportunity,” he said. “I said, it has to come back. It has to.”

Flipping means something different now than in the days when just holding a property for a few months guaranteed a profitable resale, Mangham said. “Today, we are not buying homes and flipping them. We are buying and remodeling them.”

But still, if there are too many flippers or if they are accelerating price increases, can’t that be a sign of trouble? Where is the line?

As the housing bubble burst, flips accounted for 18.2 percent of Atlanta sales. Somewhere in-between – perhaps around 10 percent – is the danger zone that signals an over-heating market, said Daren Blomquist, vice president at Attom.

"Based on the data, right now we have flippers behaving rationally, not over-speculating," he said. "Right now, it is just not a dominant force in the housing market."

The ease of getting money helped fuel out-of-control speculation leading to the eventual burst of the housing bubble, said Dan Immergluck, a professor in the Urban Studies Institute at Georgia State University. "We saw a variety of excesses. Flipping was a cause, but not the only cause."

Groundfloor’s “crowd-funding” model for flipping has the potential to push prices higher and feed speculation, but only if it were much larger in scale, he said.

In small numbers, the impulse to buy and re-sell serves a vital function – especially in depressed areas or distressed properties, Immergluck said.

For instance, the Mortimer brothers recently bought a Grant Park house that has been vacant for years. With a Groundfloor loan, they paid $120,000 for the house. They expect to sell it for about $300,000, but they intend to put in about $120,000 in improvements first.

“I hate the term flipping, hate the connotations,” Mortimer said. “We want to do it right. We are building up neighborhoods and bettering neighborhoods.”

Flippers

Median price of home purchased by flippers in Atlanta: $116,555

Median price of home sold by flippers in Atlanta: $177,000

Home “flips” as percent of total sales in Atlanta: 7.1 percent

Home “flips” as percent of total sales, nation: 6.9 percent

Source: Attom Data Solutions

Groundfloor, the company that lends to flippers

Headquarters: Atlanta

Loaned thus far: $70 million

Average loan size: $150,000

Number of properties with loans: 500, one-third of them in Atlanta

Number of investors: about 7,000

Source: Groundfloor

Share of Atlanta home sales represented by flipping

2005: 8.6 percent

2006: 14.7 percent*

2007: 14.3 percent

2008: 11.2 percent

2009: 6.5 percent

2010: 5.8 percent

2011 5.4 percent

2012 6.1 percent

2013 7.8 percent

2014 7.8 percent

2015 6.9 percent

2016 6.6 percent

2017 6.9 percent

2018 7.1 percent

*Peak was in third quarter: 18.2 percent

Source: Attom Data Solutions

Flipping as share of home sales, by county

Newton: 11.7 percent

Clayton: 9.6 percent

DeKalb: 8.4 percent

Fulton: 8.4 percent

Bartow: 7.8 percent

Cobb: 7.0 percent

Coweta: 6.8 percent

Gwinnett: 6.6 percent

Source: Attom Data Solutions

Flips as share of total sales, by ZIP code

30311, Atlanta: 18.1 percent

30032, Decatur: 16.8 percent

30310, Atlanta: 16.4 percent

30344, Atlanta: 16.1 percent

30331, Atlanta: 13.5 percent

30316, Atlanta: 13.0 percent

30016, Covington: 12.7 percent

30314, Atlanta: 12.6 percent

Source: Attom Data Solutions

About the Author

Michael E. Kanell, the AJC's economics writer, has been reporting on jobs, housing and the economy at the AJC for nearly two decades. He has appeared on television and radio to analyze and report on business and economic developments.