Opinion: Economic distortions of wealth taxes

The United States has never had a comprehensive wealth tax, and while some European countries have them, many more have repealed wealth taxes over the past several decades. That has not deterred U.S. Sen. Elizabeth Warren, D-Mass., along with U.S. Reps. Pramila Jayapal, D-Wash., and Brendan Boyle, D-Pa., from introducing legislation to create a tax on household net wealth above $50 million at a 2 percent rate per year and above $1 billion at a 3 percent rate per year, mirroring the signature policy from Warren’s presidential campaign.

Despite its proponents’ optimism, the amount of revenue a wealth tax could raise is highly uncertain, and it would cause many economic distortions and face significant implementation and administrative issues.

Sen. Warren’s wealth tax base would consist of a household’s financial and nonfinancial assets, like stocks and land, at market prices, minus a household’s debts. In addition, the 3 percent rate on net wealth above $1 billion would rise to 6 percent if legislation enacting a comprehensive health insurance program went into effect.

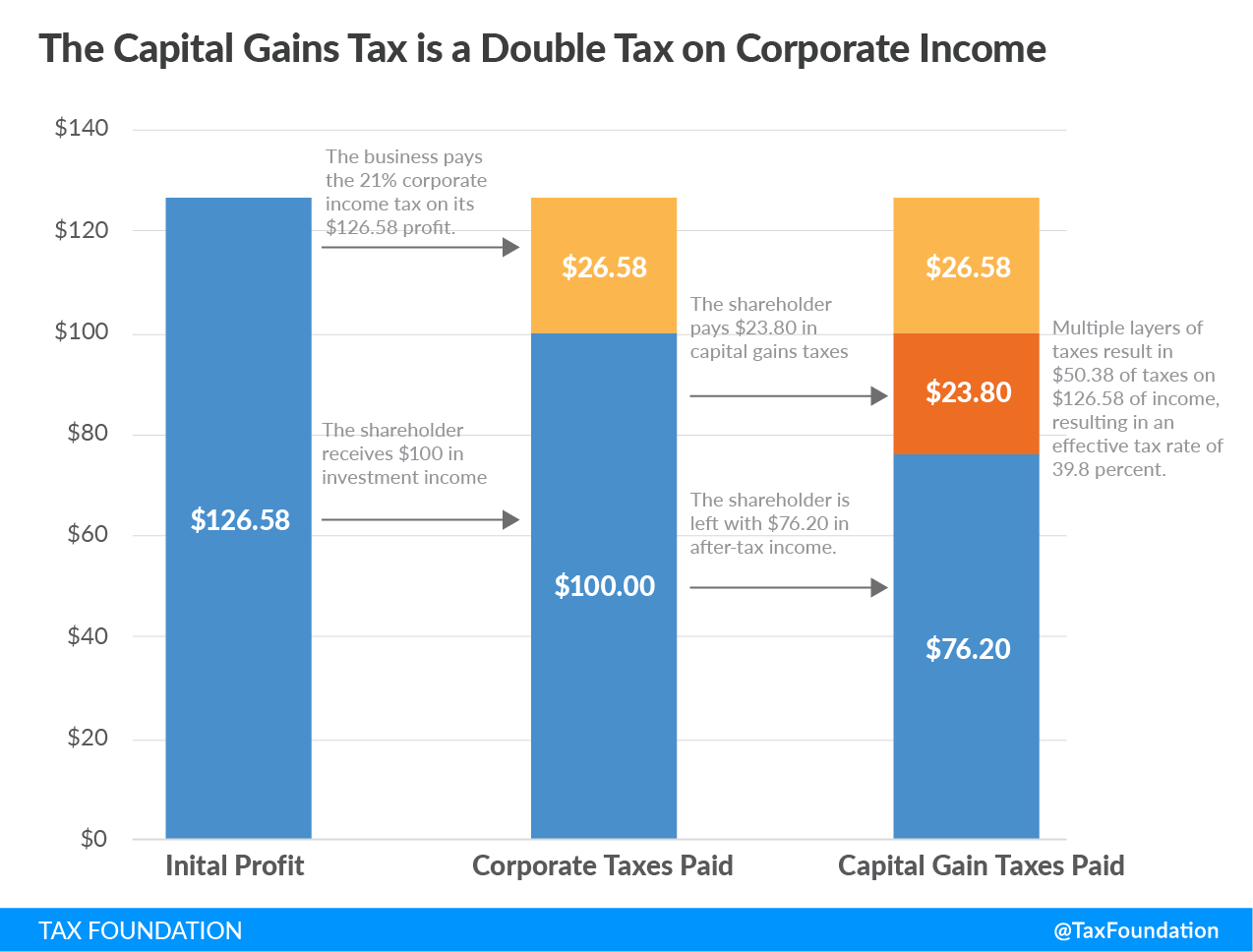

Compared to income taxes, wealth tax rates seem much lower, but that perception can be deceptive. The best way to interpret wealth tax rates is to translate them into an equivalent income tax rate. Imagine an investor who owns a long-term bond with a 5 percent fixed rate of return each year. A 3 percent annual wealth tax implies that 60 percent of the income flow from the bond would be remitted as tax. The 60 percent tax on the return to wealth would be in addition to other layers of tax that capital income faces under current law, including federal, state, and local corporate income taxes, individual income taxes on interest income, capital gains, and dividends, and estate and gift taxes.

{kind=link}

A wealth tax would place a higher burden on normal returns than on super-normal returns. In other words, someone at the margin of deciding whether to consume now or invest for the future would face a higher wealth tax burden than someone enjoying windfall returns due to monopoly power, patents, or economic “rents”, defined as returns above the normal levels that might be expected in competitive economic markets.

A wealth tax would have a negative impact on the economy. It would reduce national income, discourage saving and encourage consumption, and potentially lead to significant distortions in international capital markets as foreigners increased their investment to offset the reduction in domestic saving. In January 2020, the Tax Foundation estimated that Sen. Warren’s wealth tax would reduce national output by 0.37 percent and reduce national income by 1.15 percent in the long run.

In terms of revenue, we estimated Sen. Warren’s wealth tax would raise $2.6 trillion over 10 years on a conventional basis and $2.3 trillion on a dynamic basis, whereas she estimated it would raise $2.75 trillion over 10 years.

Estimates vary over how much revenue a wealth tax could raise. For example, Kyle Pomerleau of the American Enterprise Institute reviewed 13 publicly available revenue estimates of wealth taxes that varied from $366 billion to $5.3 trillion over 10 years. The high level of uncertainty is in part due to questions about how to value privately held assets that do not have a straightforward market price like stocks or bonds, and how such assets are distributed. The legislation leaves it to the Treasury Department to design a way to appraise hard-to-value assets.

The legislation includes $100 billion of additional funding for the Internal Revenue Service. It is not clear, however, that the IRS would be able to collect a wealth tax more efficiently than current taxes, even if resources were increased. The legislation mandates a minimum 30 percent audit rate for households subject to the tax and a 40 percent “exit tax” on net worth above $50 million on Americans who renounce citizenship. The inclusion of such stringent measures suggests a comprehensive wealth tax would be difficult to enforce.

Several countries in the Organisation for Economic Cooperation and Development (OECD), including Austria, Denmark, Germany, Finland, Iceland, Luxembourg, Ireland, and Sweden, chose to repeal their wealth tax during the last 30 years. The tax policy literature indicates reasons for repeal include limited revenue collection, administration and compliance cost, tax avoidance, and evasion. The experience of enacting and then repealing wealth taxes shows that they were not effective tools.

The international experience with wealth taxes should serve as a warning to the U.S.

A wealth tax would reduce the size of the economy, shrink national income, and significantly distort international capital flows.

It would likely raise less revenue than what Sen. Warren estimates and create large administrative challenges for the IRS.

Rather than design a new tax structure on wealth on top of existing taxes, it would be more productive to reform our current system of capital taxation and find less distortionary and administratively challenging ways to increase federal revenue.

Erica York is an economist with the Tax Foundation’s Center for Federal Tax Policy. She is also an adjunct professor at Sterling College in Kansas.

------------

Looking at anticipated impact of proposed wealth tax

Wealth taxes seek to value assets, such as publicly traded investments, for which there is a known market value. But if they seek to include ownership stakes in closely held corporations and partnerships, it’s crucial to understand that privately held business assets often defy evaluation.

Take a recent example from the tech world, where PayPal acquired an online coupon-clipping company called Honey in 2019. Before its acquisition, the 200-person company had raised about $41 million in venture capital and was likely generating good, if not necessarily phenomenal, income for its founders. After the acquisition, its two cofounders and two other high-ranking employees split $4 billion. The co-founders are both billionaires now, but would anyone have valued their assets at anywhere near that level prior to the sale? And if they had, how would the owners have been able to pay?

Taxing wealth consisting in part from unrealized gains from publicly traded assets is relatively straightforward, since some portion of the shares could be sold in satisfaction of tax liability. (This would, of course, still have consequences for some wealthy investors who are trying to maintain a controlling interest, and conflicting treatment of capital gains at the federal and state levels would create confused incentives.)

But with private business assets, the tax can be much more consequential: some portion of the company or its assets may have to be sold to pay taxes on gains that only exist on paper. The owners can be asset rich but cash poor.

This information was excerpted from a column on the Tax Foundation’s web site.