No one would buy Dele Lowman’s South Florida townhouse when she first moved to Atlanta in 2008 — not at the height of the housing crash, and not for anything close to what she paid in 2005. So she short-sold it, eating the loss on the mortgage.

Since then, she had a kid. Got married and divorced. Left Atlanta and came back.

Today, Lowman has a master’s degree, works in government consulting and is chairwoman of the DeKalb County elections board. She’s also pre-approved to buy a home.

But the ghosts of the housing crisis aren’t done haunting her.

Instead of building generational wealth through homeownership, Lowman has been thwarted at every turn by out-of-state investors who are profiting off the same crisis that wiped out the equity in her home 15 years earlier.

Metro Atlanta has become ground zero for an investor takeover of the American Dream.

Long the bedrock of family wealth for the middle class, single-family homes have been snatched up in the thousands by private equity firms and publicly traded companies, converted into rental properties and bundled into complex investment vehicles.

These firms did not create Atlanta’s affordability crisis. A generational housing shortage, inflated construction costs and a surge in consumer demand have all contributed to the historic rise in prices. But a growing body of evidence leaves little doubt that the flood of cash from investors has exacerbated it.

“They go after every listing under $500,000 … it’s like clockwork,” said Maura Neill, a realtor in Alpharetta. “The property gets listed and, sight unseen, they make offers within an hour.”

Large investment firms are pushing homeownership out of reach for many first-time buyers, an Atlanta Journal-Constitution investigation has found.

Armed with billions of dollars in cash, bulk buyers have accumulated more than 65,000 single-family homes across the Atlanta metro area over the last decade, an AJC data analysis found. Eleven companies own more than 1,000 homes each. The two largest — Invitation Homes and Progress Residential — own more than 10,000 homes apiece.

Geographically, the investor purchases form a ring around all but the wealthiest neighborhoods in the metro area, blanketing the core counties and far-flung suburbs in every direction. But disproportionately, investors buy in places with entry-level homes and in communities of color, a pattern that experts say is likely to exacerbate the racial wealth gap.

Lowman has rented two single-family homes in her Stonecrest neighborhood. Both were bought out of foreclosure by investment firms. Her current landlord, Ohio-based VineBrook Homes, bought them in early 2022 when it acquired the entire rental portfolio of nearly 3,000 homes nationwide from another private equity firm for $350 million.

Today, shell companies affiliated with VineBrook own more than 700 homes across metro Atlanta, the AJC analysis found. In 2011, that would have made VineBrook the largest single-family rental company in Atlanta. But after a decade of corporate acquisitions and mergers, VineBrook is 15th.

The AJC analyzed tax assessor data across 11 counties to identify every home purchased by investors that own more than 50 houses. AJC reporters interviewed dozens of renters, homebuyers, real estate agents, attorneys, academic experts and government officials, and reviewed hundreds of pages of public filings and corporate earnings call transcripts.

American Dream for Rent: Our Findings

Across the Sun Belt, investment firms are extracting wealth where families normally build it: the single-family home.

Since the Great Recession, large investors have snapped up more than 65,000 homes in metro Atlanta and converted them to rentals. And the flood of Wall Street cash is pushing homeownership out of reach for many middle-class families.

Investors buy in all but the wealthiest neighborhoods, but their homes are disproportionately found in African American communities.

Priced out of buying, families who wind up renting from these same firms can face deplorable conditions, exorbitant fees and frequent eviction filings by out-of-state landlords driven to maximize shareholder profits.

Metro Atlanta is ground zero for the investor takeover of the American Dream.

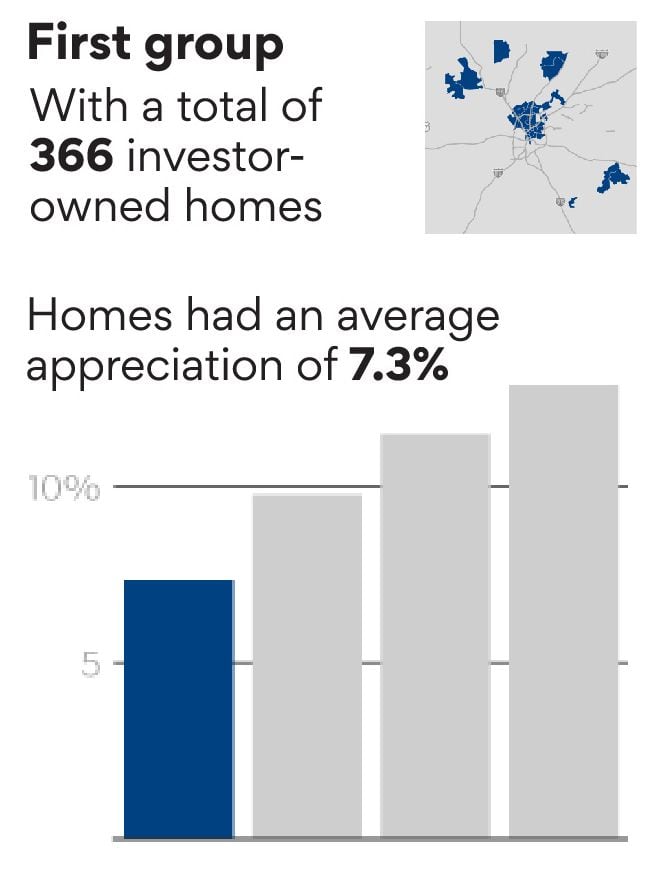

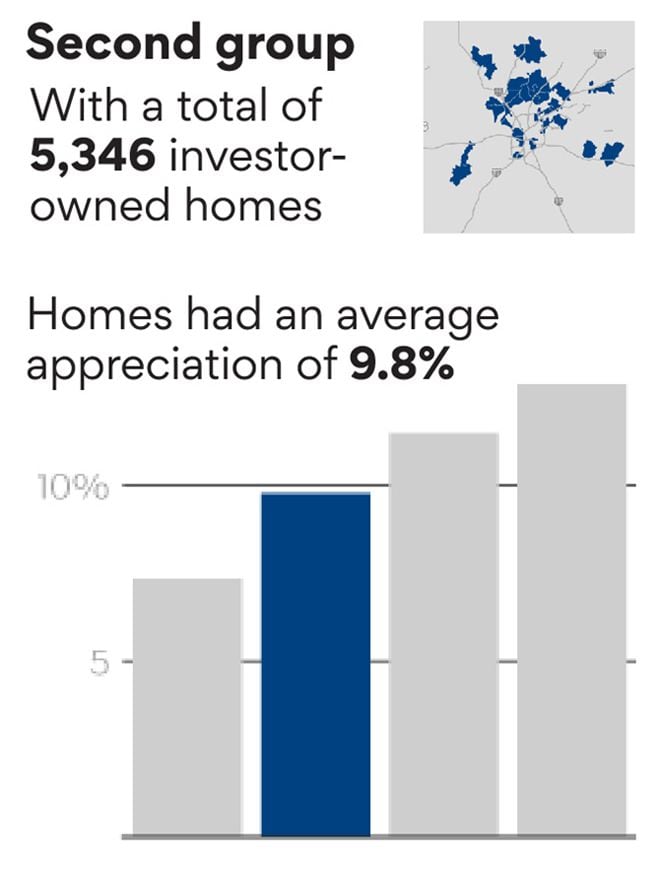

Metro Atlanta home values have risen across the board from 2012 to 2022. But the AJC’s analysis found they climbed more sharply in places where investors bought more houses. In the 30 ZIP codes with the most investor-owned properties, home values appreciated at nearly twice the annual rate as the 30 ZIP codes where investors own the least.

Experts say the effect on homeownership has been dramatic.

A landmark study from Georgia Tech found that the rise in investor activity caused a 1.4 percentage point drop in homeownership rates in metro Atlanta from 2007 to 2016. That translates to 16,500 fewer households owning homes than would be expected, were it not for the influx of Wall Street cash.

African Americans like Lowman have been hit the hardest. Investor purchases explain a 4.2 percentage point drop in Black homeownership during that period, the research found.

Large investor purchases haveaccelerated since then. During one 12-month stretch beginning in July 2021, investors bought one out of every three homes for sale in metro Atlanta.

Dele Lowman, seen on her home's front porch in October, has rented two single-family homes in her Stonecrest neighborhood. Both were bought out of foreclosure by investment firms. Her current landlord, Ohio-based VineBrook Homes, bought them in early 2022 when it acquired the entire rental portfolio of nearly 3,000 homes nationwide from another private equity firm for $350 million. (Natrice Miller/natrice.miller@ajc.com)

In public statements, industry officials deny they are a threat to homeownership, calling it a “myth” that investor activity had priced many Americans out of the housing market. They insist they are responding to the changing lifestyles of today’s workers, who sought more space when remote work disrupted the daily commute to the office.

David Howard, CEO of the National Rental Home Council, told the AJC that housing market dynamics are too complicated “to come to a consensus” on whether investors are affecting homeownership. Collectively, NRHC member companies own 450,000 single-family rental homes nationwide.

“The reality is that America needs more housing, whether that is owner-occupied housing, whether that is apartment housing, whether it’s single-family rental housing,” Howard said. “...When you have a market like Atlanta, characterized by lots of people moving there, companies expanding, you’re going to have more demand for rental housing.”

Lowman looked into buying the home on Salem Trail when she first moved in. But “the previous property manager said flat out, ‘We will not sell the property — don’t ask,’” Lowman said.

Property records tell a different story: LLC after LLC was perfectly willing to sell. Just not to a family.

One private equity firm flipped it to another, and another, before VineBrook (owned by NexPoint, an alternative investment platform) bought it in February 2022.

With each purchase, the home value rose, from $49,000 to $190,000 today. With each subsequent owner, Lowman said, maintenance got worse and her rent went up.

‘A vehicle for profits’

The air conditioning unit stopped working shortly after VineBrook bought Lowman’s rental. She says her emails and phone calls went ignored for months, even when a record-breaking June heatwave hit. Eventually, Lowman and her daughter moved to a hotel to escape the deadly heat.

“With this company, there’s no human beings — not any people with names, at least — that you can contact,” Lowman said. “We’re merely a vehicle for profits.”

VineBrook officials declined to be interviewed for the story. In a statement, a spokesperson described the company as “part of the solution to meet growing demand” for rental housing by fixing up older homes.

“We predominantly purchase homes from other investors — often with residents in place — spending an average of $25,000 to rehabilitate houses after we buy them,” the spokesperson said.

Even as industry officials publicly deny impacting homeownership, company executives deliver a different message to investors. In their initial public offering, officials for Invitation Homes, Atlanta’s top homeowner, said that government policies encouraging homeownership would directly threaten their business model.

“With this company, there's no human beings — not any people with names, at least — that you can contact."

- Dele Lowman, renter of a VineBrook home in Stonecrest

Companies also tout their ability to push rent and fees higher and higher, even as they market themselves as providers of affordable housing. Founded by Blackstone Group, a private equity giant, Invitation Homes raised its average rent in the Atlanta market 37% from $1,336 in 2016 to $1,836 today, according to public filings. It raised rent 11% in 2022 alone.

“Put simply, we see ourselves as a solution to changing preferences, demographics and housing supply demand imbalances for years to come,” Dallas Tanner, the CEO of Invitation Homes, said in a 2021 earnings call.

Tanner made $9.7 million that year in salary, stock awards and incentives — up from $5.5 million in 2020.

Company officials declined interview requests. In a statement, an Invitation spokesperson said: “We are very careful not to suggest we offer affordable housing, but we are also very clear that renting is more affordable than buying in many markets.”

Brian An, who authored the Georgia Tech study, estimated for the AJC that the drop in homeownership attributable to investors equates to more than $4 billion in lost wealth for metro Atlanta families.

“When they have investor meetings, the CFOs brag, ‘our rate of return has really increased,’” An said. “So where does that money come from? That comes from those who have lost their homes, or those that cannot move in, and even from those who have moved in as renters.”

‘We’re chasing our tail’

Every level of government had a role in helping the largest firms amass portfolios of thousands of rental homes.

Federal policies helped create the modern single-family rental industry in the wake of the 2008 housing crash, then encouraged its growth with rock-bottom interest rates and taxpayer-backed loans long after the crisis abated.

Today, large investors have moved beyond buying foreclosed homes for cheap, and actively compete against Atlanta families for starter homes.

Meanwhile, state laws make it easy for corporate landlords to maximize profits, shirk their maintenance responsibilities and evict tenants when they refuse to pay for an uninhabitable home, the AJC found. Studies show the largest single-family landlords take full advantage, raising rents and feesfaster — and evicting tenants more frequently — than small and mid-sized landlords.

Understaffed and overwhelmed, local governments have failed to use the few tools they have to hold landlords accountable.

The consequences are strewn across the Atlanta suburbs.

Raw sewage spilled for months from a Kennesaw home into a nearby creek. Faulty wiring in a Stockbridge home sparked an electrical fire in the dead of night, forcing a frightened family to evacuate. And a Florida family lost most of their $1,800 security deposit after abandoning a “move-in ready” Decatur rental that had no water or heat, active gas and carbon monoxide leaks, and a mold infestation.

Brian Morris, the code enforcement director for the city of South Fulton, said it took a year to get someone at Progress Residential to respond to complaints about trash and overgrown grass violations. Using tax assessor and deed records, the city sent certified mail to the Arizona-based LLCs that owned more than a dozen homes in a single subdivision. They also tried to contact the New York-based agent registered with the Secretary of State’s Office.

No one answered, he said.

“When we see that property go into disrepair, we’re chasing our tail,” Morris said. “All those barriers they put between us and contacting them adds weeks and weeks and weeks to the process.”

State law blocks local governments from making it easier to find landlords. In Georgia, cities can’t require themto register rentalproperties and provide a point of contact.

Morris said he finally got Progress’ attention when the city moved to clean up the mess itself and file a lien against the property. A company attorney apologized. His excuse: Progress owns more than 80,000 homes nationwide, and “we just took our eyes off this one,” Morris recalled.

Hot days, mold and ruined furniture

If any tenant could navigate the system to get results from an out-of-state landlord, it should be Lowman, a former assistant Fulton County manager with extensive ties to local government.

But she found what thousands of people in her situation do: Georgia law is not on her side.

After her air conditioning died last May, months went by without a response from VineBrook. Lowman researched her rights as a renter, and notified the company that she would make repairs herself and deduct it from her rent. She filed a code enforcement complaint July 7, and the city of Stonecrest confirmed two violations.

Meanwhile, the hot days on Salem Trail dragged on. Mold invaded the home. Lowman threw out ruined clothes, furniture and kitchen utensils. One VineBrook contractor tried to install a gas-powered air unit, only to realize the house doesn’t have gas hook-ups, she said.

Rotting paneling awaits repairs on the chimney at Dele Lowman's Stonecrest home last fall. "We're merely a vehicle for profits," she said of her landlord VineBrook. (Natrice Miller/natrice.miller@ajc.com)

Dele Lowman of Stonecrest bought this window air conditioning unit while waiting on her landlord to repair the main air conditioner, which died last May. Months went by without a response from landlord VineBrook. (Natrice Miller/natrice.miller@ajc.com)

Rotting paneling awaits repairs on the chimney at Dele Lowman's Stonecrest home last fall. "We're merely a vehicle for profits," she said of her landlord VineBrook. (Natrice Miller/natrice.miller@ajc.com)

She prepared a speech for Stonecrest Municipal Court, where she hoped to convince the judge the only way to hold a corporate giant like VineBrook accountable was to levy the maximum fine allowed under Georgia law.

“It’s $1,000 a day and they started it May 2. It’s accrued since then, so we’re already at $180,000 at this point,” or $90,000 per violation,Lowman told the AJC on Aug. 8.

That afternoon, VineBrook finally replaced her A/C unit — 98 days after it broke. But she said the company never fully addressed the mold.

On Sept. 6, the judge kicked her off the Zoom call and told her to watch on YouTube. Tenants aren’t allowed to testify against the homeowner during code enforcement hearings, Lowman was told. A company representative asked for a delay, and the judge agreed. Portfolio Manager Martin Burrow said he hadn’t been notified of the hearing in time to get an attorney.

His defense was plausible in a state that makes it hard to serve legal notice to landlords. The shell company that owns the home, “P Fin II F LLC,” is still registered to the address of a previous owner. Lowman, who had spoken with the company’s attorney about a settlement in August, found Burrow’s excuse dubious.

Dele Lowman points to stains on a dining room chair at her Stonecrest rental home in October. After going 98 days without air conditioning, excess humidity caused mold and mildew to grow on the furniture in her home. Though the air conditioning issue finally was addressed, she said the landlord, VineBrook, never fully addressed the mold. (Natrice Miller/natrice.miller@ajc.com)

On Oct. 27, VineBrook pleaded no contest to the two charges, and paid a $500 fine.

The consequences for Lowman were far worse.

She spent $2,200 on hotels and portable A/C units. When she tried to deduct the repairs from her rent, VineBrook’s online portal wouldn’t accept a penny less than the full amount. So on the same day a contractor fixed her air conditioning, VineBrook threatened to evict her if she didn’t vacate the home. Since then, she’s spent close to $4,000 to hire an attorney, wiping out much of what she had saved for a down payment.

“All that I wanted was my air conditioning to work,” Lowman said.

In an August court filing, VineBrook denied any wrongdoing. Its attorney, June James, wrote that the landlord made “timely repairs” and had not caused Lowman “unnecessary trouble and expense.”

Later, in a January statement to the AJC, a VineBrook spokesperson acknowledged the company was to blame.

“While we strive for resident satisfaction and believe average resident tenure of over four years exemplifies that overall, this is unfortunately a situation where we fell short,” the statement said. “We have worked with the resident to reach an amicable solution to this issue.”

Outcompeting homebuyers

When Natasha Dunning moved to Georgia from the Indianapolis suburbs in 2021, she and her fiancé put down offers on three homes in Henry County.

“We had the down payment, but every time it was like, ‘Oh, well, sorry the owner decided to go with a cash offer,’” Dunning said.

It’s a story that played out over and over during the pandemic, real estate agents told the AJC. And it’s not just that investors have more money.

Large firms outcompete local residents at every stage of the homebuying process, says Elora Raymond, an urban planning professor at Georgia Tech who studies investor-owned housing.

They offer all cash and a fast closing, without the risk of a mortgage falling through at the appraisal stage like it can for traditional buyers. But most still rely heavily on debt to generate enormous sums before buying. And they often borrow at lower costs than an individual.

In November 2018, VineBrook borrowed $241 million through Freddie Mac, with an adjustable interest rate. Thanks to the backing of the government-sponsored loan buyer, VineBrook’s rate was 1.66% in March 2021. The average individual mortgage rate at the time was just over 3%.

Many firms buy sight unseen and can waive inspections. Driven by algorithms, so-called iBuyers like OpenDoor and Zillow put in bids faster than any human possibly could — even with a good broker. Then they flip them again at a markup, sometimes to individuals but often to other investors.

The AJC found that bulk buyers own 9.2% of all single-family homes in the lower half of metro Atlanta census tracts, ranked by median home values. And they compete in all but the wealthiest quarter of Atlanta census tracts.

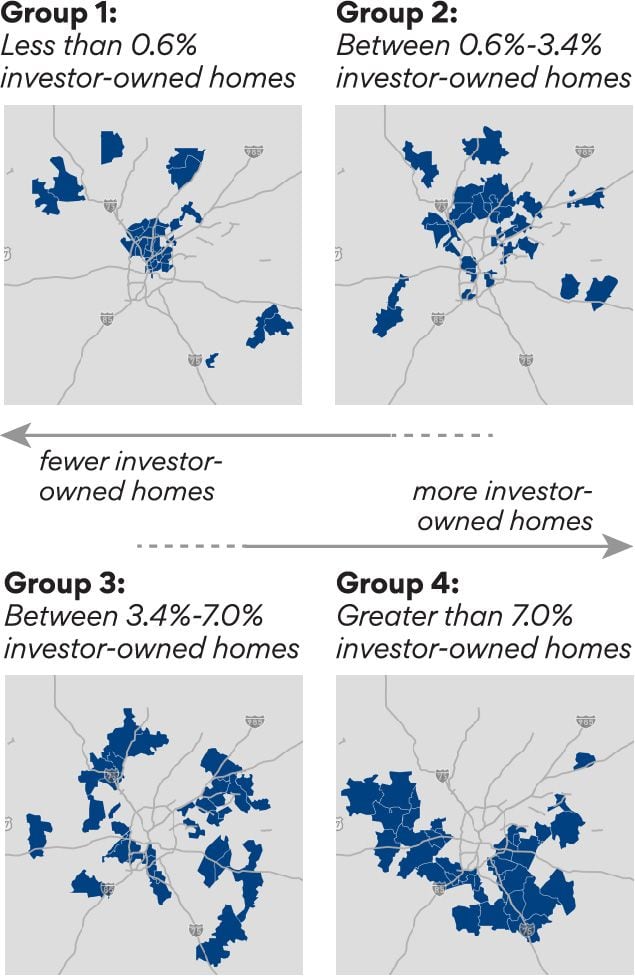

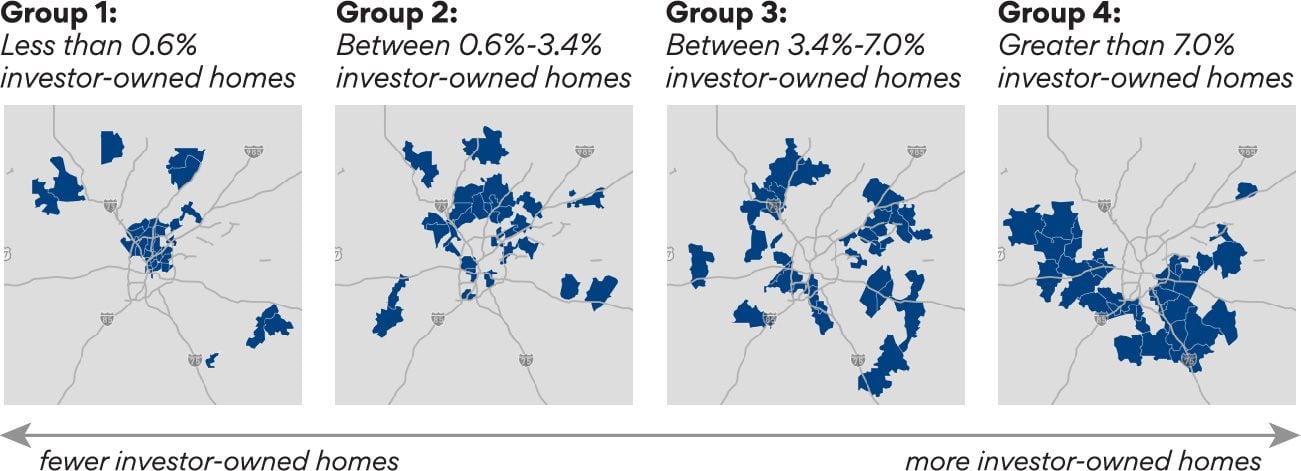

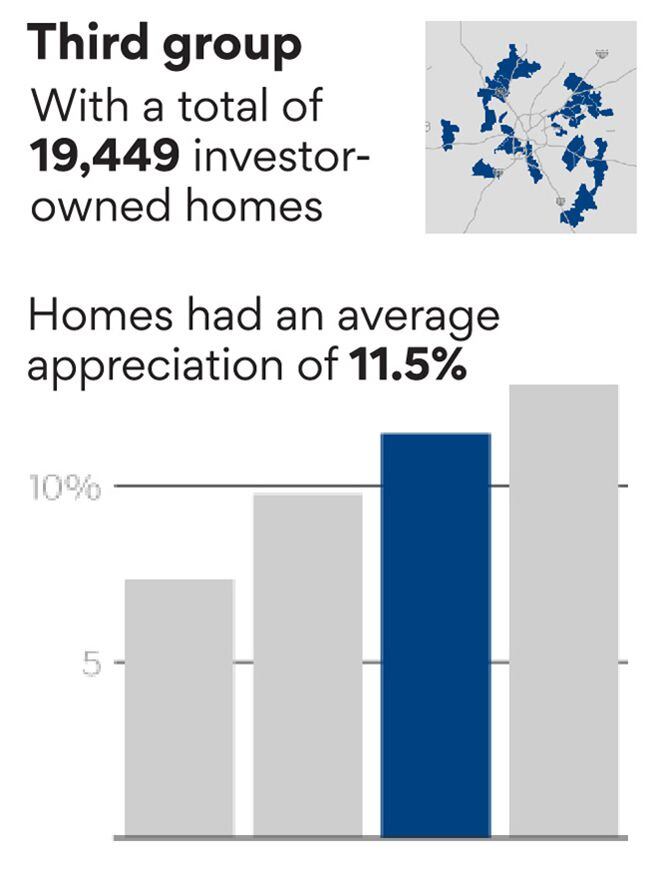

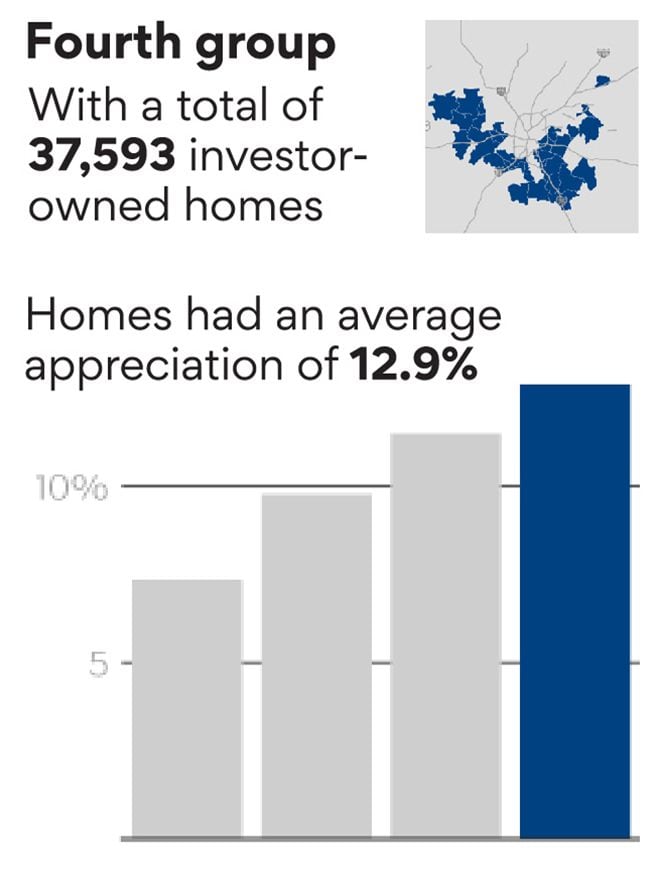

Analyzing the impact of investor-owned homes

The AJC studied nearly 150 metro Atlanta ZIP codes to determine the impact investor ownership had on home values. ZIP codes were sorted by the number of investor-owned homes and divided into quartiles of roughly 36 ZIP codes each.

Rising values: The AJC then determined the average rise in value that people saw for single-family homes in their neighborhoods between 2012-22, depending on which grouping their ZIP code is in.*

The result? As each group showed more investor-owned homes, the average appreciation in the associated ZIP codes also rose.

*Average appreciation is the average annualized increase in the ZIP code median home values, provided by Zillow, weighted by the number of single-family residential parcels in a ZIP code.

SOURCE: AJC analysis

CREDIT: John Perry, Pete Corson & Emily Merwin DiRico/The Atlanta Journal-Constitution

Some homes get snapped up before they’re ever listed.

The incessant calls, texts and letters offering cash are all too familiar to Atlanta-area homeowners. Increasingly, some firms bypass the sales market entirely, contracting with the nation’s largest homebuilders to produce build-to-rent subdivisions that are never offered to the public for sale.

At the height of the buying frenzy, Allison Kloster, an Atlanta real estate agent, recalled fielding 21 offers on one home. Nineteen were from investors.

For homebuyers, the math can seem hopeless. One of Kloster’s clients put down offers on 22 houses.

“It was hard to watch when our job is to match a family and a home,” said Kloster, of HOME Real Estate.

Rising interest rates have cooled the market considerably. But it has only solidified the primacy of cash.

In a 2022 survey, first-time homebuyers, who are more likely to need a mortgage, made up just 26% of all owner-occupied home purchases — their lowest share since the National Association of Realtors began tracking it 41 years ago. In Georgia, just 22% of buyers were purchasing their first home, the survey found.

Experts fear rental monopolies

After a decade of corporate consolidation, the six largest single-family rental firms own 63% of the homes bought by bulk buyers in metro Atlanta, the AJC’s analysis found.

And in some cases, one or two firms have the lion’s share of the single-family rental homes in a given neighborhood, raising concerns about the lack of competition.

Research suggests that the largest owners behave like monopolies that set the price of rent, rather than responding to the market. In otherwise similar neighborhoods, large landlords raise rents faster where they own a larger share of houses, a 2022 study by University of Texas at Dallas researchers found.

“That’s not supposed to happen,” said Raymond, the Georgia Tech professor. “And given how concentrated they are in Atlanta specifically, that’s scary.”

Industry officials insist they are a minor player in the U.S. housing market, telling Congress and state lawmakers across the U.S. that large companies only own 2% of single-family rental homes nationwide. That’s too small a number, they say, to affect home prices, drive up rents or prevent families from buying houses of their own.

“When they have investor meetings, the CFOs brag, ‘our rate of return has really increased.' So where does that money come from? That comes from those who have lost their homes, or those that cannot move in, and even from those who have moved in as renters."

- Brian An, who authored a Georgia Tech study on investor activity

Asked if member companies had policies to safeguard against anti-competitive behavior, Howard did not answer directly. He noted instead that the relative supply of single-family rental housing declined from 2016 to 2021 before rising again in 2022, according to census data. But that decline followed dramatic growth in the wake of the Great Recession, academic research shows.

“What’s important here is ... we need more housing,” said Howard, the National Rental Home Council CEO.

Desiree Fields, an associate professor at the University of California-Berkeley, says citing a national statistic deliberately obscures the reality in Atlanta.

“They want to minimize the appearance of having market power,” Fields said.

The largest firms only buy in a handful of markets nationwide, predominantly the Sun Belt and the Midwest, where jobs and population growth are booming,homes are relatively inexpensive and government regulations are lax.

Atlanta has been the top market for years.

Investors bought one of every three homes for sale here from July 2021 to June 2022 — the most in the country, according to real estate data firm Redfin. The largest firms bought more than twice as many homes in Atlanta as any other market in 2019 and 2020, according to the Congressional study.

Investment firms don’t just own a higher share of rental houses here than the 2% national figure would suggest — they own 5.6% of all single-family houses across metro Atlanta. At the neighborhood-level, the corporate market share is even larger. The AJC’s analysis found that large companies own at least 20% of the homes in nine metro Atlanta census tracts.

The deck was especially stacked against Dunning. Henry County is home to 11 of the 20 hottest census tracts for bulk buyers in the metro area, the AJC’s analysis found.

She ended up renting from Atlanta’s second-largest homeowner, Progress Residential, in a relationship she describes as a “hate affair.” It can take hours or days to reach a human being on the phone, she said. Maintenance requests can take weeks.

At Winslow at Eagles Landing neighborhood in McDonough, many homes are owned by investors. Two companies - Invitation Homes and Progress Residential - each owned more than 10,000 homes in metro Atlanta as of the third quarter of 2022. Henry County is home to 11 of the 20 hottest census tracts for bulk buyers in the metro area, the AJC's analysis found. (Hyosub Shin / Hyosub.Shin@ajc.com)

Progress officials declined to be interviewed. In a statement, a spokesperson said staffing and supply chain challenges during the pandemic “affected our service and maintenance timelines in some instances.” The statement said Progress made “significant investments” since then, “particularly in customer care.”

Dunning can’t wait to move when her Progress lease ends in July. The trouble is, where?

“In my neighborhood, there’s two families that actually own their homes. The rest? Down the block, that’s Progress. I’m Progress. Next door is Invitation, two homes further down are Invitation and American Homes 4 Rent homes. At the end of our block is a Progress home, and then you go to the other side and it’s Progress homes.

“You turn around and it’s Progress, Progress, Progress,” she said.

‘$500 doesn’t hurt them’

Experts say it’s no accident Atlanta has attracted investors. State law makes it easy to make money as a landlord, and hard to be a tenant.

A 2022 AJC investigation of dangerous conditions in low-income apartments found that Georgia is among the most landlord-friendly states in the country.

Dangerous Dwellings: An AJC investigation

In 2022, The Atlanta Journal-Constitution sought to uncover why so many violent crimes took place at certain apartment complexes in the city and its suburbs.

Reporters embarked on a year-long effort which included collecting crime data from 15 area law enforcement agencies and code enforcement records from 19 jurisdictions. They also analyzed lawsuits, property records, corporate documents and files from local and state housing agencies. More than 250 persistently unsafe and unhealthy apartment complexes were identified.

Last year, suburban mayors in both parties testified before the state Legislature that they need help before it’s too late. As of last spring, large investors had only deployed one-fourth of the $89 billion in capital they raised to acquire single-family homes, The Wall Street Journal reported. Even traditional mortgage lenders are getting into the game. JPMorgan Chase in November announced a $1 billion single-family rental partnership with investors.

In response, some cities now require on-site property management in build-to-rent subdivisions. A few have discussed caps on the percentage of homes that can be rented in single-family neighborhoods. But most local agencies have taken no action at all.

Morris, the South Fulton code enforcement director, plans to proactively target the largest firms’ homes to hold their owners accountable.

“That’s all they’re going to understand,” Morris said. “They’re so big that $250 doesn’t hurt them, $500 doesn’t hurt them. But if we can hit them for $10,000 every time they come to court every couple months, you’re going to feel that no matter who you are.”

Experts say it will take more than aggressive code enforcement to protect homebuyers and renters alike.

“We have a system that has enabled the creation of this industry,” Fields said. “There needs to be transformations at the local, state and national scale to turn that around.”

In Georgia, some state lawmakers are pushing for less regulation, not more.

The final report of an interim study on housing affordability shrugged off concerns about investors, and instead placed the blame for high housing costs on local regulations. “The Georgia General Assembly ... should consider legislation that will make it easier for the free market to meet the housing needs of Georgians,” concluded the report, signed by committee chairman Rep. Dale Washburn (R-Macon), a real estate broker.

A Washburn bill introduced last session would pre-empt local governments from regulating single-family rentals at all.

After eight months fighting with her landlord, Lowman worries her buying power is slipping away. Before she reached a settlement in January, theeviction hanging over her head could have made it harder to find her next home.

“It makes you feel like you’re in this by yourself and fighting against this corporate goliath,” Lowman said. “It really starts to weigh on you.”

But her consulting business is booming, and her real estate agent believes she can obtain down payment assistance. If she can put her court battles behind her, the American Dream might be attainable this year.

She had been watching the listings for a home she adores in her Stonecrest neighborhood. It could use some work, but the layout is similar to her rental. It’s the rare house under $250,000 that still remained in the hands of its longtime owner-occupant, an elderly woman.

This fall, it sold to an investment firm.

Lowman never saw it listed for sale.

— Staff writer Michael Kanell contributed to this story.

Editor’s Note: An earlier version of this story misstated the number of master’s degrees Lowman has completed.